Recently, China has successfully navigated its way up the music industry food chain, rising from 12th to 7th in the global industry in just two years. Here we look at what has led to the rapid growth in the country’s streaming and recording business,

________________________

Guest post from the Soundcharts Blog

The music business in China is a rapidly developing, vibrant industry: in just two years, it went from 12th to 7th place in the IFPI global recording market rankings, and you wouldn’t find such growth elsewhere in the world. However, what are the drivers of this development? Will the trend hold up in the future? China is one of the hottest topics in the industry right now, as music professionals all over the globe recognize the market’s vast potential. However, if you would compare to traditional, western markets, you would probably find more differences than similarities. The music industry in China faced unique challenges — and developed equally unique solutions. That is why we’ve decided to take a deep dive, and tell you everything that you need to know about the music business in China.

This article is the first chapter of our analysis, where we will explore the general structure of the market as well as the country’s recording industry. The second chapter, where we get down to the live industry and the place of international artists in China, will follow shortly, so stay tuned for that — and if you want to make sure you won’t miss it, follow Soundcharts on Twitter, where we share the articles we publish the moment they’re out.

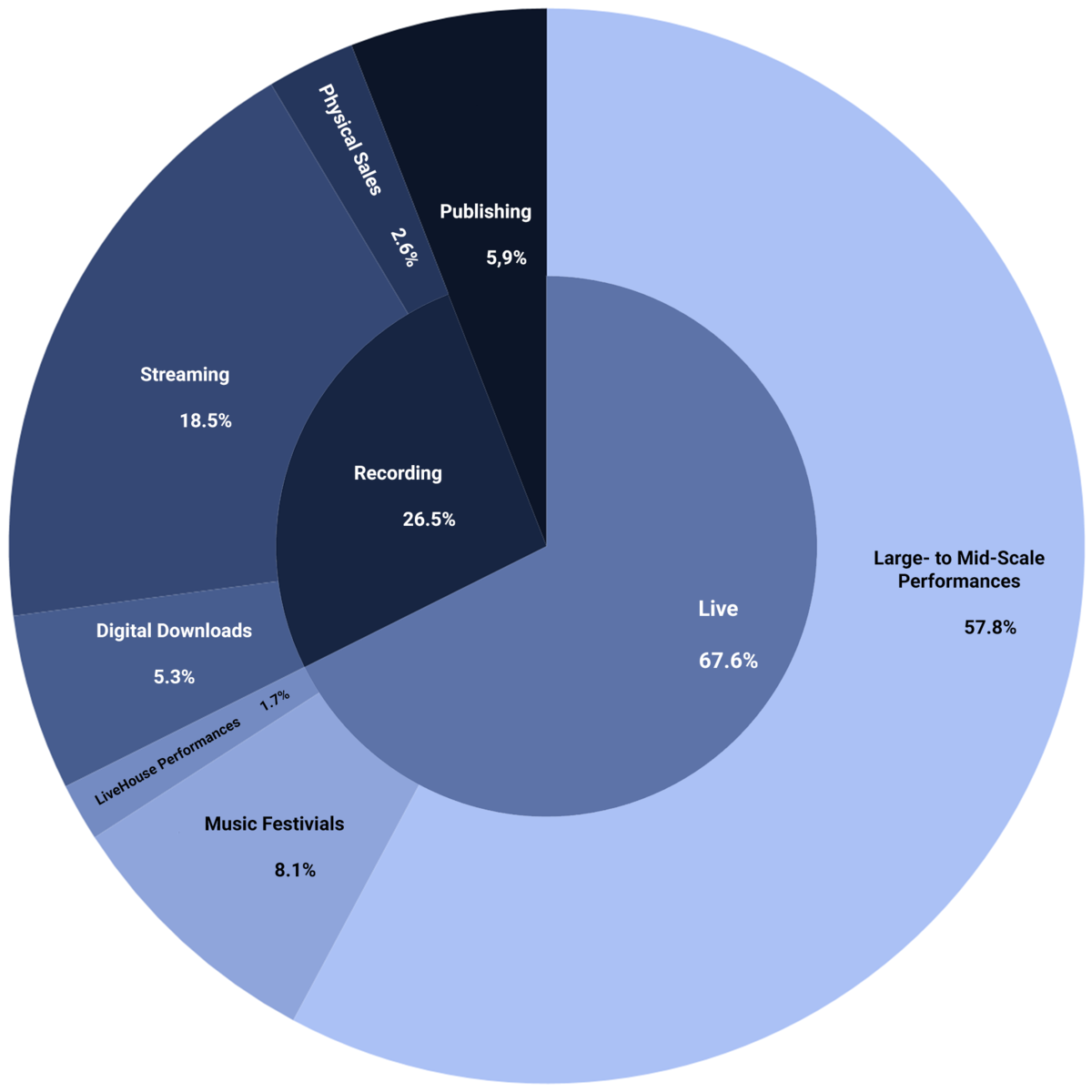

So, without further ado, let’s get into it. In line with the traditions of our Market Focus articles, we will start with a couple of key statistics across the main verticals of the local music business: Live, Recording and Publishing.

Structure of the industry and key statistics:

1. Live Industry

- Live concerts generated $747 million in 2017, up 13% from the previous year

- The number of performances reached 15,5k, attracting 13.4 million viewers, with a year-on-year increase of 30% and 14%, accordingly

- Throughout 2017, solo concerts of international artists accounted for 11.8% of the total live revenues (excluding music festivals)

2. Recording Industry

- According to IFPI data, recorded music sales generated $292.3 million in 2017, up 35.3% since 2016

- Around 70% of the recording revenues, or $205 million, was generated by steaming, while physical sales accounted for as little as 7%.

- In 2017, the number of DSPs’ users reached 523 million with the average subscription rate of about 4%

3. Publishing Industry:

- Publishing generated $65 million (Source 1, Source 2) in 2017, split halfway between the two copyright management bodies: MCSC, China’s only CMO and state-owned karaoke PRO, CAVCA

- The copyright enforcement remains problematic: reportedly, MCSC collects the royalties across less than 5% of broadcasters in China

Summarizing the revenues of 3 core sub-industries, we estimate the total revenues of the music industry in China at $1,1 billion, which is about 5% of the total scope of the U.S. music business.

Chinese Music Industry Revenue by Source, 2017

Sources: IFPI, CAVCA, MCSC, The Daolu Cultural Industry Research Center

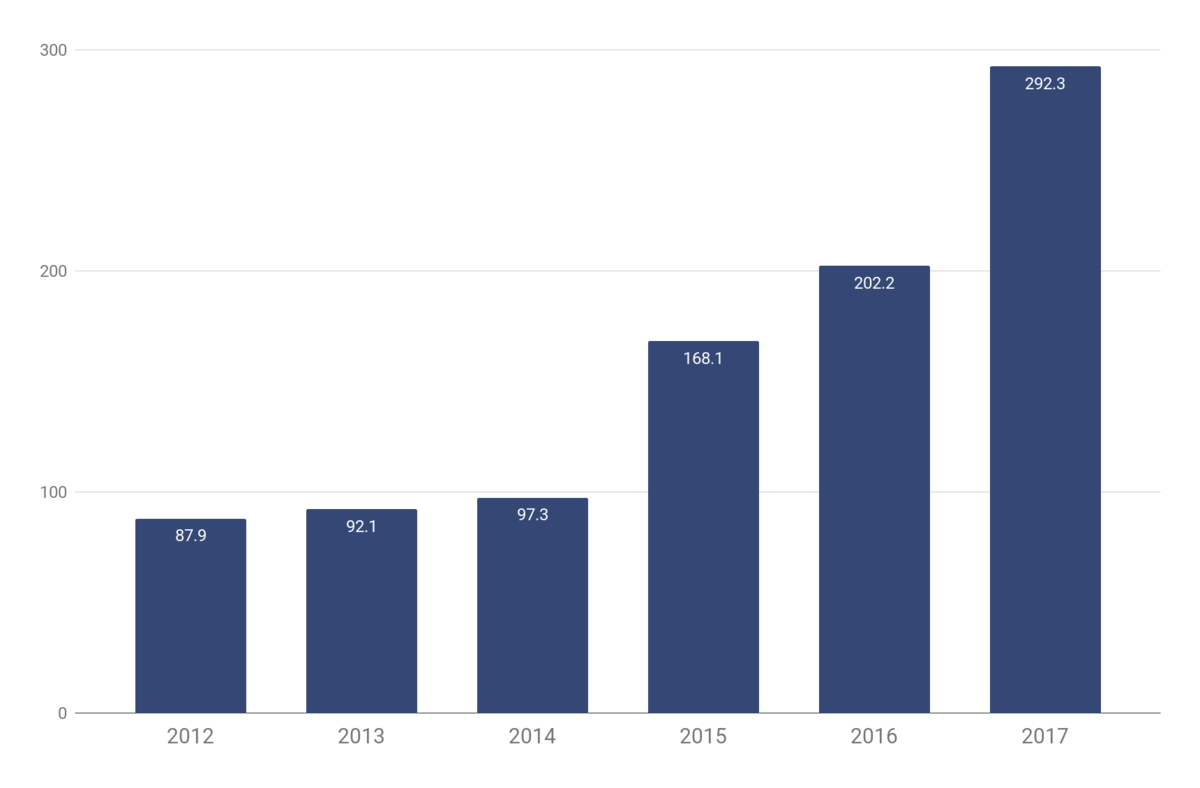

Record Industry in China

Out of all of the sub-industries, the record business is by far the fastest growing part of the market. The wholesale revenues have tripled in the course of just three years, from under 100 million in 2014 to 292.3 million in 2017. This adds up to a CAGR of 44,2% — and you wouldn’t find such growth outside of China. At the same time, the gross revenues remain very low, as the retail value of the Chinese market is about 3,3% of the U.S. record industry with its $8,7 billions in music sales. Of course, such a comparison is not really fair: the U.S. is the biggest music market in the world, at the forefront of the industry’s development. However, there are more similarities between the markets than you might think.

Recording Industry Wholesale Revenues, 2012-2017 US$ million

Source: IFPI

As we’ve mentioned in our analysis of the U.S. music market, around 75% of all recording revenues in the United States are generated by streaming, and China gets very close to that figure with its 70%. However, when it comes to actually monetizing the streams, the local services fall short of their western counterparts. In that sense, the music market in China is both mature and underdeveloped:yes, digital music dominates the consumption landscape in China — in fact, it has been that way for more than a decade — but the industry still has a long way to go until it brings in the money. Per-capita recorded music revenue in China is just $0.21, about 100 times lower than in developed markets like the U.K. and the U.S. So, even if the current CAGR holds up, the Chinese market will catch up to the U.S. $8,7 billion figures only by 2027.

At the same time, there is an ongoing debate on whether or not the current growth rate will hold up in the future. In a sense, the digital music industry in China was born just four years ago, and a significant portion of the growth we see now is due to the transition from the previous distribution models. As a result, it’s hard to predict how the market will develop going forwards, once the streaming services are adopted across the board. However, before we get into that, we need to understand the environment, in which music streaming has developed in China. To do that, let’s take a quick look at the landscape of the Chinese web in general.

Digital services in China

China is a country with the largest internet population in the world. There are over 800 million internet users in China and that huge audience remains inaccessible to most global players. The likes of Google and Facebook are banned on the Chinese web, and can’t be accessed without using a VPN. China is the only country in the world that applied protectionist policies to the local digital market, at least to such an extreme extent. The Great Firewall created a sort of digital microcosm, and we’ll have to hand it to the Chinese government — in the absence of the global competition the local analogs of the western products have flourished.

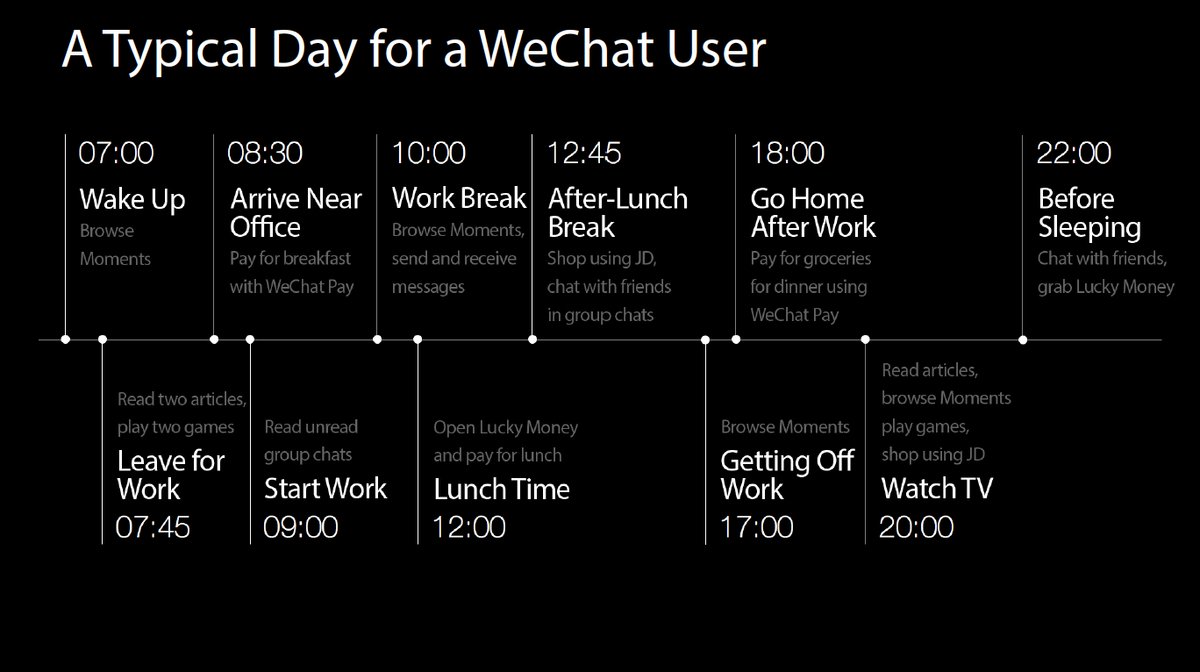

Baidu replaced Google, QQ took the place of Facebook, Alibaba became the country’s Amazon, etc. — and the corporations behind those services became the tech heavyweights of global scope. However, it would be only half-truth to say that “WeChatis a WhatsApp of China”. The fact is that, while those services mostly borrowed the core concept of their services from the west, their approach to building the product was very different. WeChat is a perfect example of this: launched in 2011 as a basic text messenger app, by 2018 it has become the super-app that you won’t find elsewhere in the world. Right now, you can pay for groceries, shop online, play games, chat with friends, send transfers — all without ever leaving the app, and that is just a part of its almost limitless functionality.

A Typical Day for a WeChat User

Source: WeChat Blog

However, let’s not get too sidetracked. The point is that China’s digital landscape was formed under the influence of two main factors: the absence of the global players and local cultural context that shaped the product philosophy. The same is true for the country’s music streaming landscape. There’s no Spotify or Deezer in Mainland China (Apple Music is available since 2015, with next to no success) — instead, the market is split between KuGou, QQ Music, KuWo, NetEase Cloud Music and alike. However, you shouldn’t see those services as copy-cats of the western streaming apps. In fact, the historical players like KuGou and KuWo (launched in 2003 and 2005, respectively) were around long before Spotify came about. Yet there’s a catch: from their launch and up to about 2015 they were what the global industry would call illegal pirate websites.

Music Piracy in China

Up until 1990, the copyright legislation simply didn’t exist in China, as it was considered unnecessary for the communist state. Throughout the 1990s, as part of China’s economic reform, the copyright law was gradually developed, and by 2001, it included even the right to stop users of P2P networks from sharing copyrighted content. However, while the copyright law was fully established by 2001, the governmental structures weren’t all that interested in actually enforcing it (at least when it came to the music copyrights). As a result, throughout the 2000s, the pirate services freely roamed the Chinese web.

Even Baidu, the Google of China, had a hugely popular MP3 search function, which aggregated hundreds of pirate websites. Baidu was brought to court multiple times by the global right holders, but the attempts were mostly ineffective. Baidu was found innocent most of the time, raising the King Kong defence, or found guilty — and charged laughable fines of 60,000 RMB, or about $8,800 (split amongst the Big Three, so around $3k each). The lack of copyright enforcement yielded predictable results — by 2011, 99% of all music downloads in China were illegal.

In 2011, things started to change. Baidu stroke a deal with all of the majors: the tech-heavyweight licensed 500,000 songs worth of catalog and agreed to revoke its MP3 search feature, replacing it with the country’s first semi-legal streaming service Ting, now known as Baidu Music (which wasn’t very successful). However, the real shift came four years later, when the Chinese government decided to intervene and enforce the copyright. It was called “operation Sword Net”, and in the course of one week, more than 2 million unlicensed songs were taken off the digital platforms. From that point on, the government kept a close watch over music piracy, andin just seven years, China went from the most piracy-heavy market in the world to the point where96% of consumers listen to licensed music.

So, in a way, legal digital music was born just four years ago — which explains the low revenues of the recording industry that we see today. Illegal services have turned the consumer to digital services, but also cultivated an environment of free music access — the general population just not used to pay for music. As a result, Chinese streaming platforms have trouble monetizing the freemium streaming model. Users tend to stick with ad-supported versions, so the conversion rates remain extremely low across all streaming platforms, at just 4%. The local streaming services interpret the low subscription rates as the sign of the market potential. However, if we look at the data, the current growth of the market is powered by the flow of new users, while the 4% subscription rate remains stable since 2015. So, the question of whether the Chinese DSPs will be able to change users minds, and get to Spotify’s 46% remains open. One can be said for sure, though: even if it will work, turning Chinese consumers to premium subscriptions will be a long game.

However, paradoxically, Tencent Music Entertainment (TME), the biggest player on the local streaming market (and a subsidiary of Chinese tech giant Tencent, the company behind QQ and WeChat) is already turning in a profit — which is something that Spotify achieved only on its 10th year on the market. However, how do you monetize music consumption in the country where music is thought to be free of charge? Well, Tencent takes a roundabout way to the wallets of its users.

Tencent Music Entertainment and the Music Pan-Entertainment Market

TME was born in 2016 after the merger of QQ Music, Tencent’s own music streaming service and China Music Corporation, which operated KuGou and KuWo, two largest historic DSPs. At the moment of merger in July 2016, the newborn TME held 56% of the streaming market, and by 2018 that share has grown to over 75%, as the three apps under the TME’s umbrella (which were all kept as separate services) amassed a total audience of over 600 million MAU, according to the company prospectus. However, the secret of Tencent’s commercial success isn’t its streaming business — in fact,only29,6% of TME’s revenues in the first half of 2018, for came from its online music vertical. The rest was generated by the company’s “music-centric social entertainment services” (MSE services for short).

Monthly Active Users Share, July 2018, by Service

Source: Questmobile, Macquarie Research

To understand what that means, we need to take a more in-depth look at the part of TME’s portfolio that lies outside of the conventional music streaming. On top of the online music services mentioned before, Tencent Music also operates “music-centric live streaming services” KuGou Live and KuWo Live, and “online karaoke social community” WeSing. The live streaming services are pretty much self-explanatory: KuGou and KuWo Live allow artists to stream their live performances (imagine Twitch.tv, reserved exclusively for music-based content). WeSing, on the other hand, is a social-based karaoke app, tapping into the popularity of KTV in China (where karaoke is a $13 billion industry), allowing its users to share their covers with friends and followers.

One way to make sense of that constellation of apps is to see it as an ecosystem. The streaming services are the backbone of it, bringing in new users, and the “side-services” of live streaming and karaoke are there to monetize that traffic. Such logic is often applied in the world of free-to-play games like Fortnite (Tencent holds a 40% stake since 2012 in Fortnite’s developer EPIC Games, by the way). The free game is a traffic magnet, and that traffic is monetized by microtransactions: in-game cosmetic items and so on. TME’s ecosystem works on the same principle — but its approach to microtransactions is deeply rooted in the Chinese culture itself.

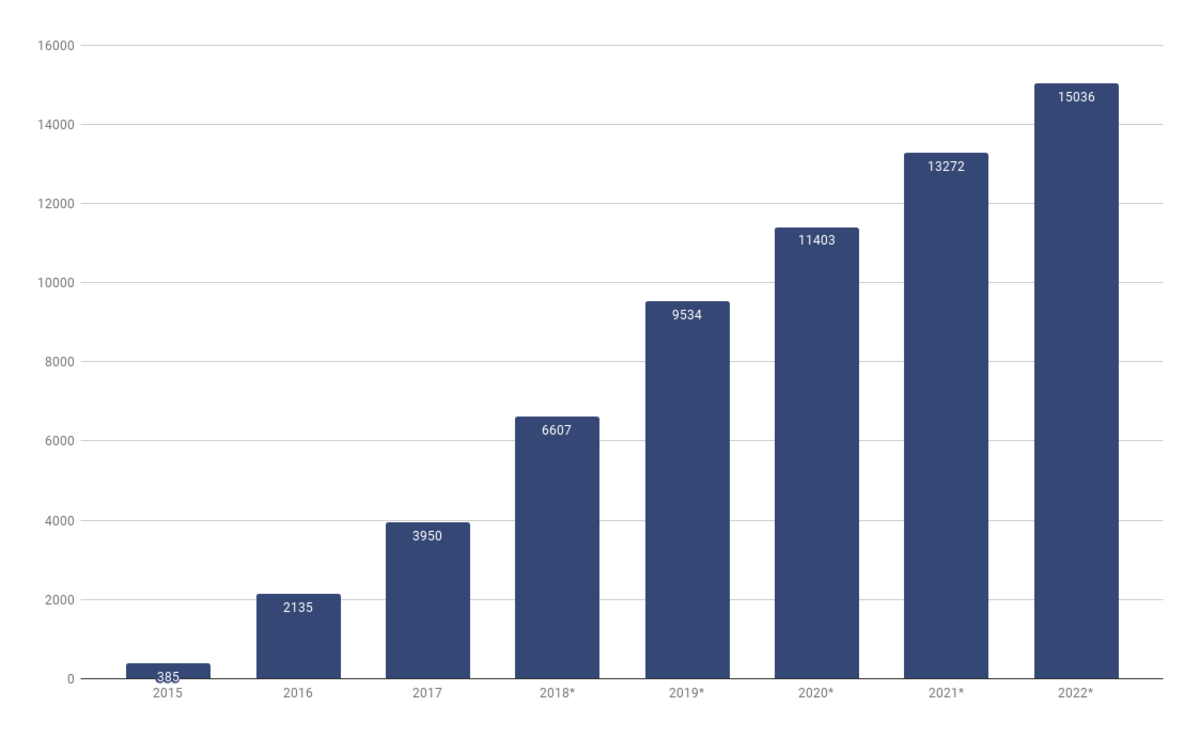

The basis of the live streaming industry in China is the “Red Envelope” tradition of gifting money to performers as a way of showing appreciation. If in the U.S. most of the revenues of Twitch are generated by ads and subscriptions, the Chinese live streaming market relies entirely on the virtual gifts and donations to streamers. That approach seems to yield great results, with live streaming in China growing at over 100% CAGR from 2012 to 2017.

Live Streaming Revenue in China, 2015-2022, $US billion

Source: Tencent Music Entertainment Group, iResearch

Tencent’s Music MSE services are built on the same principle of virtual gift-giving. The user is brought into the TME’s ecosystem by the free music streaming — but the actual money is made on the virtual gifts they would send to the performers. To put it in perspective, in Q2 of 2018, TME was making $1,27 per month on each of the 23,3 million paying users of its online music services. Over the same period,an average paying user of WeSing or KuWo/KuGou live spent almost 13 times more on virtual diamonds flying over the live-feed, as the MSE services’ 9,5 million paying users brought a monthly ARPU of $16,37.

The scope of the Music-Centric Social Entertainment Services

Not so long ago Coachella and YouTube made headlines, as the first weekend of U.S. festival broke the records by generating 82.9 million live views on the platform in the course of two days. Well, what if I tell you that the performances of Childish Gambino, BLACKPINK, Billie Eilish and alike, all combined still fall short of a single TFBOYSconcert, celebrating the four-year anniversary of the Chinese boys-band? The performance, live-streamed across all of the apps in Tencent’s ecosystem, gathered, according to Tencent,a total of 118 million live views, peaking at 7.66 million concurrent viewers, with over 340 million virtual gifts sent out during the stream. The gifts are priced in a range from 0.05 to 1000+ RMB, and even if we assume the cost of an average donation at 0.5 RMB ($0.073), that would still make about $25,000,000 pie split between TME and TFBOYS — which is about as much as Ed Sheeran made in gross ticket sales over 4 nights at Wembley Stadium last year.

Perhaps the most interesting question here is, how do you actually qualify that revenue from the artist point of view? On the one hand, the whole system is powered by streaming as the primary traffic source, so the recording industry still plays a vital role in the value chain. On the other hand, the content that actually triggers the donations and gift-giving is a live performance — although it’s pretty far from the western convention of how the concert industry makes money.

Perhaps the answer is neither. The MSE services carve out the space between the live and recording industries, but they aren’t focused on the master recording or live experience. What the TME’s “Streaming” excels at is monetizing the fandom, and in that sense, MSE services are a digital analog of the Japanese CD-based business models, that work on the same principles of turning fan-engagement into hard cash. The fact is that the two countries, despite their political tensions, have a lot in common. Just like in Japan, the fandom culture and the idol-system dominate Chinese mainstream music. Just like in Japan, you can find the stories of passionate fans buying huge ad-spaces, at home or overseas to celebrate their idols. Japanese AKB48’s business model, that we’ve explored in detail in our Market Focus: Japan, had huge success on the Chinese market, spawning 3 idol super-groups: SNH48, BEJ48 and GNZ48, based in Shanghai, Beijing and Guangzhou, accordingly. Even if the approach to actually turning the fan’s attention into money is different, the core cultural drivers behind it are the same.

Of course, not every artist on the market can succeed within the TME’s monetization model. TFBOYS’ concert is an extreme case of TME’s system in action, that is unreachable for the mid-class artists. TFBOYS are one of the most prominent artists in China right now — the band’s member Wang Junkai, for example, holds the Guinness World Record for the most shared post on Weibo (Chinese analog of Twitter) with over 43 million “retweets”. The revenue of a mid-sized artist would be nowhere near the $25 million figures. Furthermore, if you take a quick look at the content that is live-streamed on KuGou Live, you won’t find that much in terms of the actual live performances, in the western sense. More likely, you will catch something along the lines of music talk-shows: ever-cheerful hosts, laugh sound-effects and audiences applauding on cue. The fact is that, while Tencent uses the MSE services as the main way to monetize it’s streaming empire, the artists that can engage with the platform are either top-tier performers like TFBOYS, or the aspiring pop-idols, trying to build up their following. At the same time, if we take a look at the “physical’ live industry, pop music accounts for only 11% of shows in China — so it’s about 90% of artists that are left out on the curb of the TME live-streaming services.

The rest of the industry can still make money on plain streaming, right? Well, if we take MSE out of the equation, the scope of the recording industry is not there yet. Making real money from streaming is hard — if not impossible — for most of the artists on the market. TME’s per-stream payout, for example, is just 0.001 RMB, or $0.00015, which is about 3,4% of what Spotify pays the artist. Of course, TME has nearly six times more users than Spotify, which helps level out the field a bit — but still, it’s $150 made on a million of streams.

Alternatives to Tencent’s Music Empire

When the recording doesn’t bring in the money for artists, the answer is universal across the globe: treat the master as a promotion tool, and focus on other sources of revenue. That mindset has become the basis of positioning for the first challenger of Tencent on the streaming market — NetEase Cloud Music.

Remember how Apple Music had a built-in direct artist-to-fan communication channel with its Connect and Spotify used to play around with in-app messaging? Music is a social phenomenon, and so the idea of social media functionality was floating around the streaming market for a long time, yet none of the western companies had any success with it.NetEase, however, makes social features the core of it’s streaming offer — to the point where it’s hard to tell if it’s a streaming service or music-based social media.

You can find everything from comments and likes to user-generated music reviews and in-app Twitteresque microblogging on NetEase Cloud Music, and that social media functionality creates clear value for developing artists in China: NetEase is a platform where you can build an audience and directly connect with fans. There’s a reason why social media is a core of the artist development, and by building one into the streaming platform, NetEase created something of a hub for both local and international artists, trying to make it big in China.

This focus on the alternative music scene allowed NetEase to carve out a niche on the market (well, if you can call 116 million monthly active users a niche), by marketing towards a younger, urban demographics (people of 15-35 years old, living in tier-1 and tier-2 cities are the main audience of the platform). NetEase has developing artists in search of an audience on one side of its offer, and a passionate, “heavy consumption” user base on the other. Bringing those audiences together, NCM has become a staple for the non-pop music industry in China. For example, Reportedly, NetEase played a significant role in the development of EDM in China, opening up the market to some of the biggest names in dance music, and even signing direct deals with some of the top-tier international acts in the genre. When it comes to global artists, the company proudly states that over 30% of all activities on the platform — including streams, comments, reviews and everything in between — is linked to the foreign artists. That might not seem like a lot, but only until you consider the share of international artists across the market: in live industry, for example, only 11,4% of revenues in 2017 came from international acts.

When it comes to the financial model, NetEase falls closer to the likes of Spotify, relying on direct monetisation via paid subscriptions, digital album sales, advertising and so forth. However, much like Spotify, the company has little success with the conventional streaming model in terms of profitability: as of Q4 2018, NetEase has reported -5,2% gross profit margin across its music services business segment. At the same time, give the service’s positioning, NCM can’t really take the same shortcut to profitability, as TME did. As the industry insiders put it:

“It is difficult to image preponderant independent musicians on NetEase Cloud Music committing themselves to live-streaming, which is embarrassing and may not bring user flow. Diving into the live-streaming sector means NetEase Cloud Music has run out of options.”

The Future of the Recording Business

So, the streaming market in China is defined by a clear opposition of “mainstream” streaming of Tencent, relying on side-products to monetise the free music streaming, and a more westernised NetEase Cloud Music, which, while not making money for artists directly, offers musicians a huge promotion platform — especially when it comes to alternative genres and international artists. The future of the streaming remains unclear, as the main question remains open:will Tencent, NetEase and alike convert their free music consumers into paying subscribers?

However, If a couple of years ago, the main word to describe the Chinese recorded music was “untapped potential”, in 2019, it would be more like “somewhat-tapped potential”. China is steadily climbing the IFPI revenue charts, landing on the 7th placein 2018; Financial Report for Q1 of 2019, recently released by TME shows some shifts in regards to premium subscriptions, with conversion rate bumping up to 4,3%. Just recently, the news broke out that China overtook the U.S. in terms of the smart speaker sales — and, as we know, smart speakers consumption tend to drive the sales of premium streaming subscriptions. In short, the Chinese recording industry starts to mature, but it hasn’t reached the scope where middle-class artists can rely on music sales to pay the bills yet.

So, while the penetration of free streaming made the recording industry the central customer-facing part of the business, artists have to rely on other sources of income to actually make the money. However, how do you monetize your music on the market where consumers are not used to paying for it? What is the landscape of the live industry, and what are the pitfalls of planning a tour in China? Find out on the second part of our analysis, where we get down to the country’s rapidly developing live industry, and the opportunities of the Chinese concert market.

Take me to the Analysis of the Chinese Live Industry